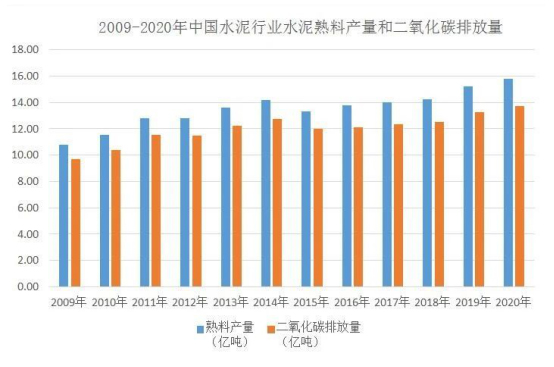

The "Administrative Measures for Carbon Emissions Trading (Trial)" will come into effect on 1st . Feb, 2021. China’s National Carbon Emissions Trading System (National Carbon Market) will be officially put into operation. The cement industry produces approximately 7% of global emissions of carbon dioxide. In 2020, China's cement output is 2.38 billion tons, accounting for more than 50% of the global cement output. The production and sales of cement and clinker products have ranked first in the world for many years. China's cement industry is a key industry for carbon dioxide emissions, accounting for more than 13% of the country's carbon dioxide emissions. Under the background of carbon peak and carbon neutrality, the cement industry is facing severe challenges; at the same time, the cement industry has carried out work such as raw fuel substitution, energy saving and carbon reduction, and industry self-discipline to continuously improve environmental quality. This is another opportunity for the high-quality and sustainable development of the industry.

The "Administrative Measures for Carbon Emissions Trading (Trial)" will come into effect on 1st . Feb, 2021. China’s National Carbon Emissions Trading System (National Carbon Market) will be officially put into operation. The cement industry produces approximately 7% of global emissions of carbon dioxide. In 2020, China's cement output is 2.38 billion tons, accounting for more than 50% of the global cement output. The production and sales of cement and clinker products have ranked first in the world for many years. China's cement industry is a key industry for carbon dioxide emissions, accounting for more than 13% of the country's carbon dioxide emissions. Under the background of carbon peak and carbon neutrality, the cement industry is facing severe challenges; at the same time, the cement industry has carried out work such as raw fuel substitution, energy saving and carbon reduction, and industry self-discipline to continuously improve environmental quality. This is another opportunity for the high-quality and sustainable development of the industry.

Severe challenges

The cement industry is a cyclical industry. The cement industry is the vane of national economic development. Cement consumption and output are closely related to the national economy and social development, especially the infrastructure construction, major projects, fixed asset investment real estate, and urban and rural markets. Cement has a short shelf life. Basically, cement terminal suppliers produce and sell according to market demand. The market demand for cement exists objectively. When the economic situation is good and the market demand is strong, cement consumption will increase. After infrastructure construction is basically completed and major projects are successively implemented, when China's national economy and society have reached a relatively mature stage, the cement demand will naturally enter the plateau period, and the corresponding cement production will also enter the plateau period. The industry’s judgment that the cement industry can achieve carbon peaks by 2030 is not only consistent with General Secretary Xi’s explicit proposal to achieve carbon peaks by 2030 and carbon neutrality by 2060, but also with the pace of adjustment of the cement industry’s industrial structure and market.

Opportunities

At present, energy consumption and carbon dioxide emissions per unit of GDP have been reduced by 13.5% and 18% respectively, which have been included in the main economic and social development goals during the "14th Five-Year Plan" period. At present, the State Council and relevant departments have also issued a series of relevant policy documents such as green and low-carbon, climate change and carbon emission trading, which has a relatively positive impact on the cement industry.

With the advancement of carbon peak and carbon neutrality, the cement industry will actively combine the development and construction needs of various periods, adjust cement production and supply according to market demand, and gradually reduce inefficient production capacity on the basis of ensuring market supply. This will accelerate the elimination of outdated production capacity in the cement industry, further optimize the layout of production capacity. Also enterprises are forced to transform and upgrade, apply new technologies and equipment to improve energy conservation and emission reduction levels, optimize resource allocation, and promote quality and efficiency improvements. The introduction of policies related to carbon peaks and carbon neutrality will also help promote cooperation between enterprises, mergers and reorganizations, etc.. In the future, the advantages of large groups will be more prominent. They will further strengthen technological innovation, increase the rate of substitution of raw materials and fuels, participate more actively in carbon asset management, and pay more attention to energy-saving and emission-reduction technologies, carbon markets, carbon assets and other information, so as to increase market competition.

The carbon reduction measures

At present, all domestic cement companies have adopted the new dry production technology, which is at the international advanced level as a whole. According to the analysis of the current situation of the industry, the cement industry has limited room for carbon reduction through existing energy-saving and alternative limestone raw material technologies (due to huge consumption and limited alternative resources). In the critical period of the next five years, the average reduction in carbon emissions per unit of cement will reach 5%, which requires tremendous efforts. To achieve the goal of carbon neutrality and CSI to achieve a 40% reduction in carbon per unit of cement, disruptive technologies are needed cement industry.

There are many literatures and reviews in the industry discussing carbon reduction through energy-saving technologies. Based on the development of the cement and concrete industry and national conditions, some experts discussed and summarized the key emission reduction measures of the cement industry: scientific and efficient use of cement by adjusting the structure of cement products; strengthening top-level design, and perfecting the responsibilities of producers and consumers” carbon emission accounting methods and various liability apportionment methods.

It is currently in the policy adjustment period. With the advancement of carbon peak and carbon neutrality work, relevant departments have successively introduced carbon emission control and related industrial policies, plans and emission reduction measures. The cement industry will usher in a more stable development situation, to drive a large number of energy-saving and environmental protection equipment and related services-based industries.

Sources: China Building Materials News; Polaris Atmosphere Net; Yi Carbon Home

Post time: Jan-06-2022